for you and your business

☰ Menu

- Home

- About

- People

- Services

- International

- Contact

- Work with us

- Blog

- Testimonials

- Resources & Downloads

- Videos

- Newsletters

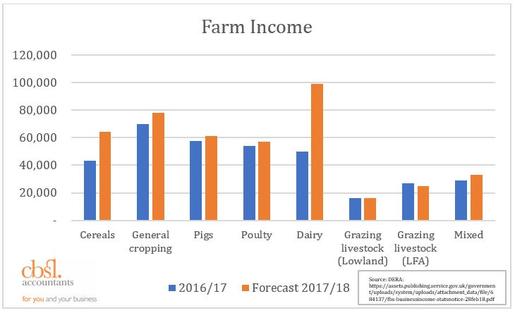

The most recent estimates of farm business income from Defra (now in its 17th year) forecast increases in farming profits across most sectors, with dairy topping the league for 2017/18. The improvement in dairy is through higher milk process and output resulting in a near doubling of profits.

The worst performing farms are again expected to be grazing livestock; less favoured areas (LFA’s) performing better than lowland, as a result of higher Basic Payments and Agri-Environment payments. Both types of grazing consistently lose money without direct payments.

The worst performing farms are again expected to be grazing livestock; less favoured areas (LFA’s) performing better than lowland, as a result of higher Basic Payments and Agri-Environment payments. Both types of grazing consistently lose money without direct payments.

Average Basic Payment s are expected to be around 6% higher across all farm types as a result of weaker Sterling exchange rates when the payments were determined.

General cropping incomes are expected to increase by 11%, with increased output from cereals, oilseed rape and sugar beet partially offset by lower potato prices. Input costs are also expected to increase, particularly crop variable costs.

Similar cost increases are expected in poultry farming, as well as reductions in the price of eggs. However, the sector is due to show a 5% increase as a result of higher poultry meat prices plus increased production of broilers, and egg production.

Brexit effects?

This is still a big question that no-one knows the answer to. Agricultural trade is though characterised by protectionism. Of all types of faming Sheep is a net exporter and so failure to get an agreement will affect this area the most.

We see the biggest effect as being on the availability of labour, and most notably in horticulture, where approximately 90% of the workforce are EU migrants. The hit is two-fold: (i) Exchange rates changed dramatically after the referendum, and so the desire to travel to the UK for a season has diminished; and, (ii) the introduction of stricter controls on inward migration will prevent some of those who do to, from coming. Migration impact on other areas such as arable, will be negligible.

What about the weather?

The DEFRA farm income data was published 28 February 2018, based on survey responses earlier in the year. They will therefore not predict the impact of the Beast from the East in late February / early March, nor the Mini-beast that followed, nor the unprecedented levels of rainfall that we have had. This is naturally having an impact on feed prices, and at the time of writing lamb prices are currently still very strong.

Farm Business Income forecasts do though tend to be reliable, with Dairy the only sector in the equivalent 2017 forecast being out of tolerance, as a result of over estimation of input costs, particularly feed. Hopefully higher dairy prices will negate this, and indeed they have increased the level they had reached when we last discussed them in this blog.

We look forward to revisiting this topic at the end of the year.